Your credit score is just a three-digit number, but it holds immense power. Like our Social Security numbers, our credit scores follow us through most of our adult lives. In fact, most of us spend more time building our credit scores than we do building romantic relationships.

March is National Credit Education Month, a campaign launched in 1989 by the National Foundation for Credit Counseling. The event is intended to promote financial literacy and help consumers understand and improve their credit scores so they can manage debt more effectively. (It’s also a timely reminder to reassess our post-holiday credit balances and do a little financial spring cleaning before the year picks up momentum.)

If you don’t already know how your credit score measures up, now is a great time to get familiar with your number and check for changes. By keeping track of your credit history, you can not only build and maintain a good credit score but also catch and address any potential issues before they become catastrophic.

The Real-World Impact of Your Credit Score

Your credit score may not affect your day-to-day life as directly as your bank balance, but it plays a major role in your overall financial well-being. That’s because, for better or worse, your credit history can determine whether you qualify for a loan or credit card, whether you can buy a home, and how much you’ll pay in interest when you do. Put simply, your credit score helps shape how expensive it is to borrow money and how smoothly you move through major financial milestones.

Your credit score is based on your credit report, which is a record of your borrowing and repayment history. It includes identifying information (such as your address and date of birth) along with details about how you manage credit accounts, late payments, collections, or bankruptcies. Three credit reporting agencies—Experian, Equifax, and TransUnion—collect and compile this data.

But what makes this three-digit number so influential goes way beyond loan and credit approval. A stronger credit score can help you qualify for lower interest rates on mortgages, auto loans, and personal loans, potentially saving you thousands of dollars over time. Credit card issuers may offer higher limits, better rewards, and more favorable terms to borrowers with established credit. Those with lower scores may still qualify for credit, but typically at higher rates or with fewer benefits. In other words, the more consistently you’ve demonstrated responsible credit use, the less you tend to pay to borrow.

Landlords also tend to review credit history when evaluating rental applications, and some employers—particularly when hiring for positions involving financial responsibility—may review credit reports as part of the hiring process.

Over time, strong credit can create more financial flexibility, while weaker credit can make already expensive decisions even more costly.

How it Starts

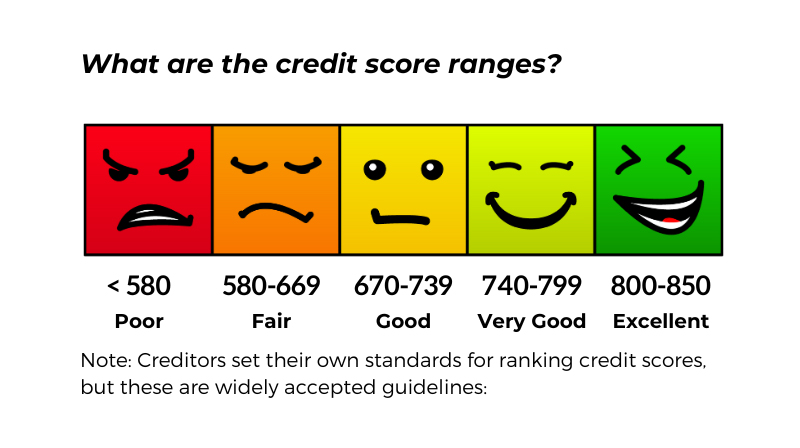

Everyone’s journey is different, but most of us get our first credit score within 6 months of taking on our first debt—either as a borrower ourselves or as an authorized user on someone else’s account. You don’t start at zero. (In fact, most scoring models range from 300 to 850.) Before you open a credit account, you simply don’t have a score at all.

Once you begin using credit—making payments, carrying balances, applying for new accounts—that activity is reported to the credit bureaus and used to calculate your score. From there, your number will rise or fall based on how you manage those accounts over time.

When you have no credit history, lenders view you as an unknown (a.k.a., a high-risk). Without a track record, they can’t easily predict how likely you are to repay what you borrow. Having no credit isn’t the same as having poor credit, but it can still make approval more difficult. Building credit is ultimately about establishing a pattern of responsible borrowing and repayment.

Tips to Improve Your Credit Score

1. Pay Your Bills on Time

Timely payments are the most important factor in determining your credit score and late payments can remain on your credit report for up to seven years. Set up reminders or automatic payments to ensure you never miss a due date.

2. Reduce Credit Card Balances

Credit utilization is typically the second most influential factor in your score. It measures how much of your available credit you’re using, and is usually calculated per card and overall. For example, if you have one card with a $10,000 limit and owe $5,000, your utilization on that card is 50%. If you have two $10,000 limit cards, each with a $5,000 balance, your overall utilization would be 25%. Many experts recommend keeping your per-card utilization below 30%, though lower is generally better.

3. Don’t Close Old Accounts

The length of your credit history matters because keeping old, well-managed accounts open will showcase your creditworthiness over time. When you pay off a high-balance credit card, it may be tempting to close the account, but there is value in keeping a zero-balance card open—especially if that account is one of your oldest accounts.

That’s because the older your average credit age, the more reliable you appear to lenders. Plus, if you choose to close an account, it will lower your overall credit limit, which also increases your credit utilization rate. Either way, the payment history on those paid-off loans and credit cards will still factor into your credit history—possibly for as long as 10 years. Positive payment history on closed accounts can remain on your credit report for up to 10 years.

4. Diversify Your Credit Mix

Having a mix of credit types (e.g., credit cards, mortgages, auto loans) can positively impact your credit score. There are two main types of credit: revolving and installment. Revolving credit is credit with an upper limit (such as a credit card or home equity line of credit, a.k.a., a HELOC). With revolving loans, when you pay down your balance, you can use that credit line again. Installment loans are loans in which you receive a lump sum and then repay it in regular installments over time (such as an auto loan, student loan, or mortgage). A mix of credit types can help, but only if it makes sense for your financial situation. Never open an account solely to improve your score.

5. Limit New Credit Applications

Increasing and diversifying your credit can help increase your credit score but it’s even more important to be thoughtful about opening new accounts. Initiating multiple credit inquiries (often called “hard inquiries” or “hard pulls”) within a short period can lower your credit score. Be selective and deliberate when applying for new credit.

6. Negotiate with Creditors

If you’re struggling with payments, consider negotiating with your creditors for lower interest rates, a payment plan, or a settlement amount. Just be sure to get an agreement in writing before making payments.

7. Ask for a Credit Limit Increase

When your credit limit goes up, but your balance stays the same, your overall credit utilization rate goes down—and that can improve your credit score. So, if your income has recently gone up or you’ve had a few successive years of positive credit experience, you have a good shot at getting approved for a higher limit. However, before you request an increase, give some thought to how you’ll keep your spending habits steady. If you think you might be tempted to spend that extra available credit, this might not be the best strategy for you.

8. Get a Secured Credit Card or Become an Authorized User

If you have bad credit or no credit, a secured credit card may be just what you need to build a positive credit history. They are often easier to secure because you pay a cash deposit upfront, and your credit limit is then equal to (and backed by) the cash deposit or savings account.

If you don’t have the means to secure a new loan or credit card, consider asking a trusted friend or relative who has a credit card account if you can be added as an authorized user. They don’t have to let you use the card (or even give you the account number) for your credit to improve as long as they have (and maintain) a good history of on-time payments. This is sometimes known as “credit piggybacking.”

9. Check Your Credit Report Regularly

Check your credit report regularly (at least once or twice a year) to monitor improvements and unexpected changes. You can access free credit reports weekly from all three major credit reporting agencies through AnnualCreditReport.com. Checking your own credit report or score does not hurt your credit, so it’s worth doing regularly—even if you’re not actively trying to improve it.

How to Monitor Your Credit Score

To track progress and spot fraud early, review your credit report regularly. Consistent monitoring allows you to adjust your habits and prevent small issues from turning into larger setbacks.

When reviewing your report, look for unfamiliar accounts, incorrect balances, and late payments you don’t recognize. Check your personal information to make sure it’s accurate. If something doesn’t look right, dispute the errors with the credit reporting agency.

And, if you’re working to rebuild poor credit, pay special attention to patterns. Are late payments becoming less frequent? Are balances trending downward? Is old negative information nearing the seven-year mark? Remember that credit improvement rarely happens overnight, and consistency matters more than quick fixes.

In addition to reviewing your full credit report weekly through AnnualCreditReport.com, you can also monitor your credit score through digital tools offered by Experian, Equifax, TransUnion, or the online credit service, Credit Karma. While the score you see through such services may not be the exact version a lender uses, the estimated score can help you spot trends and identify sudden changes.

For better or worse, your credit score reflects your financial health. That’s why building and maintaining a good credit score is such a crucial step toward achieving financial stability. By being proactive and informed, you can improve your credit score and open up a world of opportunities.

If you need help, talk to someone in our lending department or get FREE financial counseling from our partners at GreenPath Financial Wellness. As a Maps member, you have access to free one-on-one financial counseling, debt management services, and personalized credit report reviews.